TL;DR:

- Sustainable profit growth requires deliberate planning, sequencing improvements, and honest measurement.

- Operational efficiencies, pricing strategies, and working capital management are essential drivers of increased margins.

Profit growth sounds straightforward until you are actually running a business. You are managing people, chasing invoices, handling customers, and somewhere in the middle of all that, you are supposed to be growing your margins too. The reality is that sustainable step by step profit growth does not happen by accident. It happens through deliberate planning, sequenced execution, and honest measurement. This guide walks you through exactly that. From diagnosing where you stand today, to pricing with confidence and managing working capital, every step is designed to compound on the last one.

Table of Contents

- Key takeaways

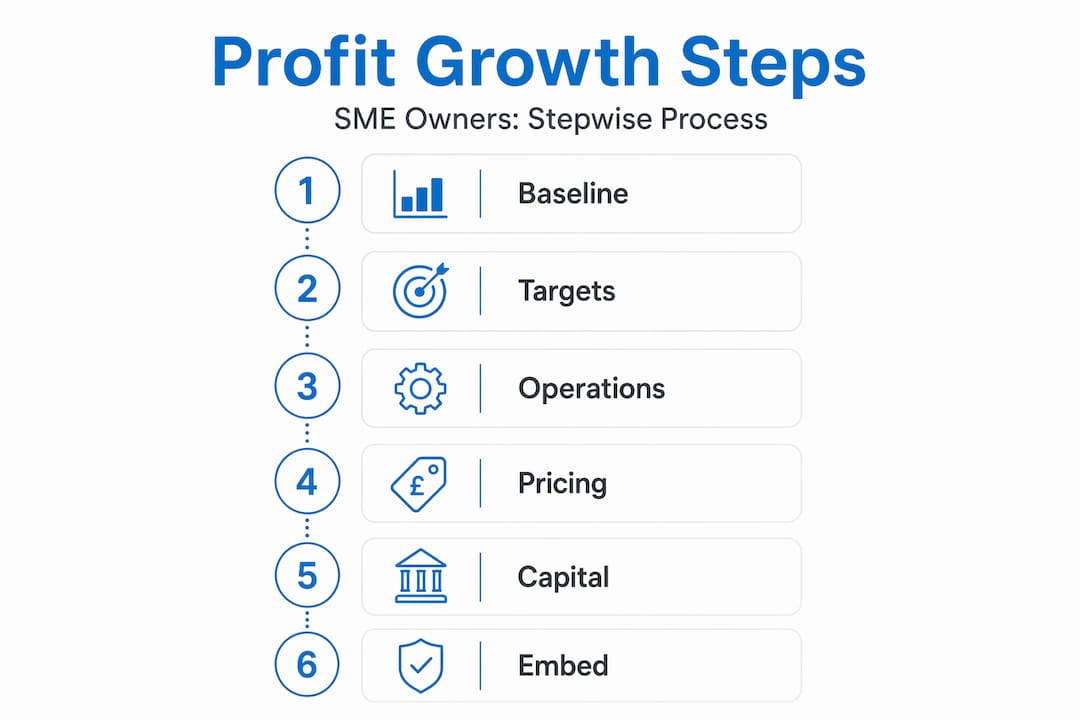

- Step by step profit growth: where to begin

- Operational improvements that move the margin needle

- Pricing as a lever for profit growth

- Working capital: the hidden profit engine

- Embedding profit growth into your business rhythm

- My perspective: what I have learned about stepwise profit growth

- Ready to accelerate your profit growth?

- FAQ

Key takeaways

| Point | Details |

|---|---|

| Start with a clear baseline | Assess your margins, cash flow, and cost structure before setting any growth targets. |

| Sequence your improvements | Operational changes, pricing adjustments, and capital optimisation work best when applied in order. |

| Pricing is your fastest lever | Even a modest price increase drops directly to the bottom line faster than volume growth ever will. |

| Working capital unlocks reinvestment | Freeing up cash tied in inventory or slow receivables gives you fuel for high-return initiatives. |

| Measurement drives results | Monthly reviews of leading and lagging KPIs keep your profit plan alive and responsive. |

Step by step profit growth: where to begin

Before you can grow profit, you need to know exactly where it is being lost. That means turning the mirror around on your business and looking honestly at the numbers. Many business owners focus on revenue because it feels exciting, but profit measurement by driver tells you far more. Revenue quality, cost to serve, and working capital efficiency are the three lenses that reveal what is actually happening.

Start by pulling together your gross margin by product line or service type. You may discover that your busiest service is also your least profitable. That is a common and costly surprise.

Here is what to assess at the outset:

- Gross profit margin per product, service, or customer segment

- Fixed versus variable cost breakdown and where costs are growing faster than revenue

- Cash conversion cycle: how long it takes to turn sales into actual cash in the bank

- Revenue concentration risk: are more than 40% of revenues coming from one or two clients?

Once you have this picture, you can set targets that are grounded in reality rather than optimism. Effective business growth plans typically cover a 12 to 36 month horizon and use scenario modelling, with base, conservative, and aggressive projections, to account for uncertainty.

| Scenario | Revenue growth target | Margin improvement target |

|---|---|---|

| Conservative | 5% | 1.5% |

| Base case | 10% | 3% |

| Aggressive | 18% | 5.5% |

Pro Tip: Do not set a single profit target. Set three. Having a conservative floor gives you confidence under pressure, while an aggressive ceiling keeps you stretching.

This diagnostic phase is where most business owners skip ahead too quickly. They want solutions before they understand the problem. Resist that impulse. The clearer your starting point, the more precise your profit plan will be.

Operational improvements that move the margin needle

Here is something that surprises most people: over 50% of potential margin improvement in many businesses comes from fixing operational inefficiencies, not from cutting costs. There is a meaningful difference between those two approaches. Cost cutting is blunt. Operational improvement is surgical.

The place to begin is with your productive unit. This is the core unit of output your business delivers, whether that is a completed job, a delivered order, a client session, or a processed transaction. Once you know your productive unit, you can measure how efficiently you are producing it and where time or resource is being wasted.

A simple waste audit covers four areas:

- Rework and errors: What percentage of your outputs require correction, follow-up, or complaint resolution? Even a 3% rework rate on a £500,000 revenue base costs £15,000 in lost labour alone.

- Waiting time and handoffs: Where do jobs stall between team members or departments? Gaps in workflow are invisible profit drains.

- Over-servicing: Are you delivering more than clients are paying for? Scope creep is one of the most common margin killers in service businesses.

- Underutilised capacity: Are staff or equipment idle during peak hours or between projects? Idle capacity costs money without generating return.

Once you identify the waste, sequence your quick wins by two criteria: speed of implementation and cost of change. Changes that are fast and cheap go first. More complex fixes, like new systems or restructured teams, get planned into the next quarter.

Pro Tip: Run your waste audit as a team exercise, not a solo analysis. The people doing the work every day know exactly where the friction lives. You just need to ask them.

Establishing a simple operational scorecard with three to five metrics reviewed weekly will do more for margin than any one-off cost review. Improvements in scheduling and dispatch efficiency alone have helped service businesses increase revenue without adding headcount. The gains are there. You just need a system to find and hold them.

For a broader view of how these improvements fit into profitable scaling strategies, it helps to see operations as the foundation every other growth lever sits on.

Pricing as a lever for profit growth

Most business owners are undercharging. That is not a guess. It is a pattern that appears repeatedly across industries when owners finally examine what their market will actually bear versus what they have been charging out of habit or fear.

Here is the reality of value-based pricing. A 2% price increase on a £1 million revenue business adds £20,000 directly to your bottom line without any additional work, staff, or overhead. Contrast that with chasing £20,000 in new revenue, which requires marketing spend, sales effort, and delivery cost. Operations and pricing levers compound each other, potentially doubling EBITDA improvements over 12 to 18 months when applied together.

The practical steps for pricing improvement look like this:

- Segment your customers by profitability, not just by revenue. Some of your highest-revenue clients are your lowest-margin clients because of support intensity or discount history.

- Audit your discounting habits. If anyone on your team can authorise a discount without approval, you are leaking margin. Implement a simple approval workflow for any discount above 5%.

- Test price increases on new work first. Raising prices on renewals or long-term clients requires care. Introducing new pricing on new quotes or new service packages carries far less risk.

- Reframe your pricing language. Clients do not pay for time or effort. They pay for outcomes. If your proposals are built around hours or deliverables, rephrasing them around results will shift the perceived value.

The fear of losing clients when raising prices is real but almost always overstated. Most clients who genuinely value what you do will stay. Those who leave were almost certainly your least profitable anyway.

Pro Tip: Before raising prices across the board, identify your top five most profitable clients and ask yourself what you do differently for them. That answer usually reveals the value you should be charging everyone else for.

Working capital: the hidden profit engine

Working capital is the cash that keeps your business running between the moment you spend money and the moment you collect it. Most SME owners think of it as an accounting concept. In practice, it is a direct profit lever.

Here is a comparison of two businesses with identical revenue and operating costs:

| Working capital factor | Business A | Business B |

|---|---|---|

| Debtor days (how long clients take to pay) | 45 days | 22 days |

| Stock holding period | 60 days | 30 days |

| Creditor days (time to pay suppliers) | 20 days | 45 days |

| Net working capital pressure | High | Low |

| Cash available for reinvestment | Minimal | Significant |

Business B does not earn more. It collects faster, holds less stock, and pays suppliers later. That discipline creates cash that can be reinvested in growth. Inventory reduction funded new equipment for one business in exactly this way, driving 15% revenue growth from capital that had previously been sitting idle on shelves.

To improve your working capital position, apply ABC analysis to your inventory. Classify stock into A items (high value, low volume), B items (moderate), and C items (low value, high volume). Reduce safety stock levels on C items first. Negotiate extended payment terms with your top three suppliers. Send invoices the same day work is delivered and follow up on overdue accounts within 48 hours, not 30 days.

Monitor working capital monthly alongside your profitability metrics. The two are inseparable when you are pursuing long-term profit growth.

Embedding profit growth into your business rhythm

A profit plan with no rhythm dies quietly. The difference between businesses that grow profits consistently and those that stay stuck is not intelligence or resources. It is the discipline of regular review. Tracking leading and lagging KPIs prevents you from reacting to problems that were weeks in the making.

Here is how to build that rhythm into your business:

- Weekly: Review three to five operational metrics. These are your leading indicators, things like jobs completed, conversion rate, and average transaction value.

- Monthly: Review profit by segment, cash position, working capital cycle, and progress against quarterly milestones.

- Quarterly: Conduct a full review of your growth plan. Adjust targets, reassign ownership of initiatives that are stalling, and celebrate what is working.

Assign clear ownership to every initiative on your profit plan. If no one person is accountable, nothing moves. Use a simple one-page scorecard that anyone in your leadership team can read in under five minutes. Planning capacity and systems before demand increases is what separates businesses that scale cleanly from those that grow into chaos.

Pro Tip: Hold your monthly profit review at a fixed time each month, not whenever it feels convenient. Profit discipline is a habit, and habits need anchors.

The goal is to make profit awareness part of your culture, not just your calendar. When your team understands how their daily decisions affect the margin, you have built something genuinely durable.

My perspective: what I have learned about stepwise profit growth

What I have seen working with SME owners is that the ones who grow profits consistently are rarely the most ambitious. They are the most methodical.

The businesses that chase big revenue wins without fixing their unit economics end up earning more while keeping less. It is one of the most demoralising patterns I encounter. You can read more about why a profitability framework that decomposes profit into its component drivers is so much more useful than a top-line growth target alone.

What I have learned is this: sequence matters enormously. Fixing operations before changing prices means your improved delivery justifies the higher rate. Improving working capital before reinvesting means you are growing with cash you already own, not borrowed money you are hoping to repay.

The most common pitfall I see is treating profit decline as a revenue problem when it is almost always an efficiency or pricing problem. Chasing more clients when your cost-to-serve is too high just amplifies the loss.

Clear ownership and a consistent measurement rhythm are not management theory. They are the practical engine of sustainable profit improvements. Build the habit, hold the rhythm, and the results will follow.

— Shane

Ready to accelerate your profit growth?

Understanding the steps is one thing. Executing them consistently while running a business is another challenge entirely. That is where having the right support makes all the difference.

At Summitscale, we work with small and medium-sized business owners who are serious about building profit with clarity and confidence. Our coaching programmes are designed to guide you through exactly the kind of stepwise improvements covered in this article, from operational tightening to pricing discipline and working capital mastery. If you want a clear plan, consistent accountability, and a coach who has been through this process with businesses like yours, explore how coaching drives SME growth or learn more about why coaching accelerates profit. Book your free 15-minute assessment call today and take the first real step.

FAQ

What is step by step profit growth?

Step by step profit growth is the practice of improving business profitability through sequenced, incremental changes to operations, pricing, and capital management rather than pursuing large, high-risk changes all at once.

How quickly can I expect to see profit improvements?

Operations and pricing improvements can compound to deliver meaningful EBITDA gains within 12 to 18 months when applied in sequence, with some operational quick wins visible within the first 90 days.

Why is pricing more powerful than increasing sales volume?

A price increase flows directly to your bottom line without additional delivery cost, whereas new revenue always carries variable costs. Even a 2% increase on £1 million in revenue generates £20,000 in pure profit.

What working capital metric should I watch first?

Debtor days is the most immediate lever for most SMEs. Reducing the time between invoicing and payment frees cash quickly and without any operational change.

How do I keep a profit plan alive over time?

Assign clear ownership to each initiative, hold a fixed monthly profit review, and track both leading indicators like conversion rate and lagging indicators like net margin to catch problems before they compound.